What Is DeFi Yield, and How Does It Really Work?

Have you ever seen a crypto website advertising 10%, 50%, or even 200% returns from DeFi (decentralized finance), and wondered where that money comes from?

You are not alone.

Yield is one of the most talked-about concepts in decentralized finance, and one of the most misunderstood. In simple terms, yield is extra crypto you earn just by holding or putting your crypto to work — similar to how a savings account pays interest, or a rental property gives you rent.

In this article, we have DeFi Yield explained — from where it comes from to how to evaluate it safely. Let’s break it down!

What Is DeFi Yield?

DeFi Yield Meaning: Simple Definition

Yield in DeFi is the return you earn by putting crypto assets to work in a decentralized protocol.

Instead of just holding tokens in a wallet, you deposit them into a smart contract — a self-running program on the blockchain that automatically handles transactions — and you receive a reward. This reward comes from helping a network or protocol in a certain way by locking your crypto. For example, staking locks your coins to help secure a particular network. Lending your crypto to lending protocols provides funds for borrowers.

Think of it like earning interest — except there is no bank in the middle!

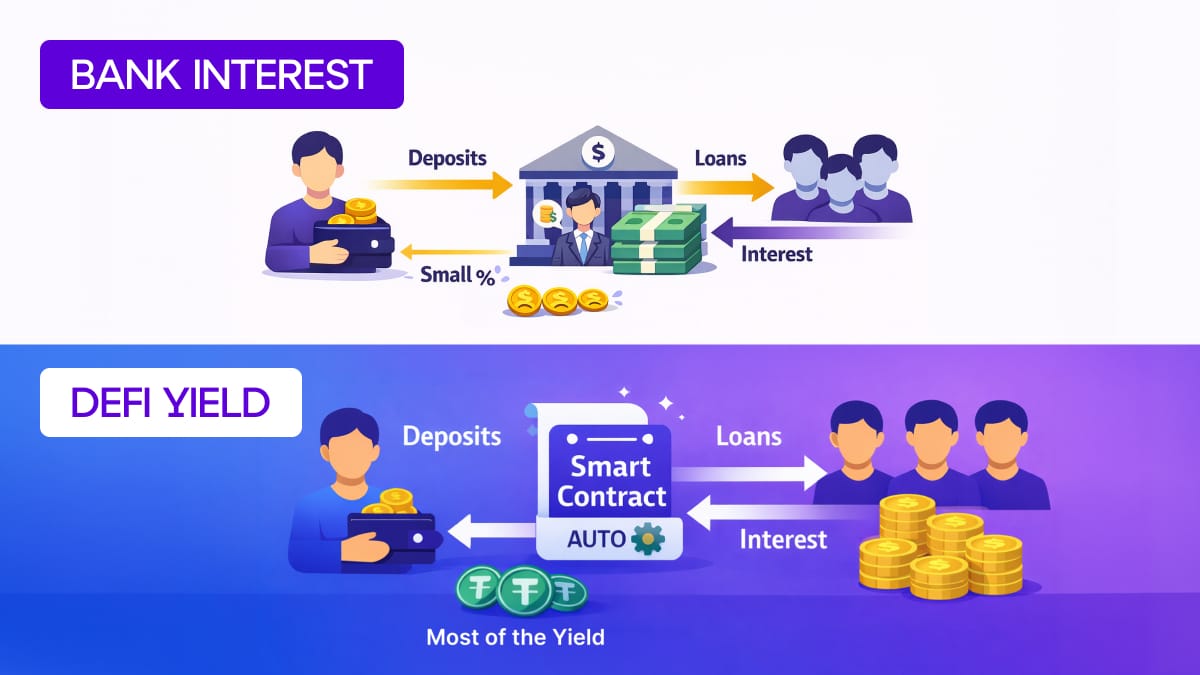

Yield vs. Bank Interest

In traditional finance, you deposit money, and the bank lends it to others, paying you just a small fraction of the interest it collects. DeFi works on the same principle, but removes the middleman.

Instead of banks, smart contracts handle everything, interest rates adjust based on supply and demand, and the process is open to anyone with a crypto wallet.

Why Does Yield Exist in DeFi?

Crypto yield exists because crypto is always in demand. Traders swap tokens, and for that, they need liquidity: they want to easily and quickly buy and sell crypto without changing its price too much.

Borrowers lock up crypto as collateral, or a security deposit, to trade with leverage — this means they can make much larger trades than they could with their own crypto. Protocols need deposits to function: without user deposits, the services simply can't operate.

A lending protocol with no deposits has nothing to lend. A liquidity pool with no tokens can't facilitate trades. User deposits are the raw material that makes these systems work — and yield is what protocols pay to attract those deposits.

To sum up, yield is the price the market pays to attract that capital.

Where Does DeFi Yield Come From?

When you see a DeFi platform advertising yields — whether 5% or 500% — it's not magic internet money. Those percentages come from real people paying for real services. And unlike traditional finance where the details are hidden, good DeFi protocols show you exactly where the returns come from.

Here are some examples:

Traders Paying Liquidity Fees

A decentralized exchange (DEX) relies on liquidity pools: they are large shared pools of tokens, locked in a smart contract. Liquidity pools make trading easy, fast, and always available — because the tokens you need are already sitting there, ready to trade. You swap directly with the pool, not with another person, so there's no waiting.

Unlike old centralized exchanges with order books, where each buyer and seller had to be matched manually, DEXs (like Uniswap) allow you to instantly swap tokens. If it weren’t for liquidity pools, trading would be slow and annoying; on top of that, the price would change instantly and you’d end up losing crypto!

These pools are funded by users called liquidity providers, who receive fees for providing that liquidity to traders. This means when you lock your crypto in that liquidity pool, you’re essentially making life easier for traders. So when a trader swaps tokens, they pay a small fee (typically 0.05–0.3%), distributed to those liquidity providers.

Borrowers Paying Interest

Another way of earning yield is by depositing crypto into lending protocols. Lending protocols are like automated money-lending systems. They let users borrow crypto by locking collateral. Borrowers pay interest, and that interest goes to users who deposit crypto into these lending protocols.Basically, doing this gives those protocols crypto which they can then lend to those who want to borrow it.

Protocol Incentives and Emissions

Beyond the fees and interest mentioned above, many protocols add an extra layer of DeFi rewards to attract users — especially in their early stages.

Many protocols distribute their own governance tokens: special crypto coins that allow you to vote on how a project or protocol runs — kind of like owning shares in a company. When you provide liquidity or lend crypto, you don’t just earn fees or interest — you also receive these tokens as a bonus.

Here’s why this matters: governance tokens often have real market value and can be sold. A protocol might advertise “100% APY” when in reality, only 10% comes from actual fees or borrowing interest, and the remaining 90% comes from these token rewards. This strategy helps new protocols grow quickly by making their yields look extremely attractive.

However, there's a catch: as the protocol mints (creates) more tokens and distributes them to users, the supply increases. If demand doesn't keep up, the token price falls — meaning the value of your rewards shrinks even though you're receiving the same number of tokens. This is why those eye-catching triple-digit yields often don't last. The advertised rate can be misleading if it relies heavily on token emissions rather than sustainable fee-based income.

Main Types of DeFi Yield

Staking Rewards

You lock tokens in a proof-of-stake blockchain — a system where your deposited tokens act as a guarantee that you'll behave honestly, helping keep the network secure.

As a reward, you receive newly minted tokens or transaction fees. Think of it this way: by locking your tokens, you become part of the network's security team.

The blockchain needs people like you to keep it running smoothly and safely. In exchange for this commitment and the work you're helping perform, the network compensates you with newly minted tokens or transaction fees.

Lending Yield

You deposit tokens into a lending pool and earn DeFi interest paid by borrowers. Rates rise and fall with borrowing demand.

Liquidity Pool Fees

You provide a pair of tokens to a decentralized exchange and earn a share of every trade fee the pool generates.

Why a pair? Because traders need both sides of the trade available. If someone wants to swap ETH for USDC, the pool must hold both ETH and USDC. As a liquidity provider, you deposit both tokens (typically in equal value, like a 50/50 split), and in return, you earn a portion of the fees from every trade that uses your liquidity.

Liquidity Mining Incentives

This practice is also commonly known as yield farming — earning bonus tokens by providing liquidity to a protocol. Such incentives are usually temporary and designed to attract early users.

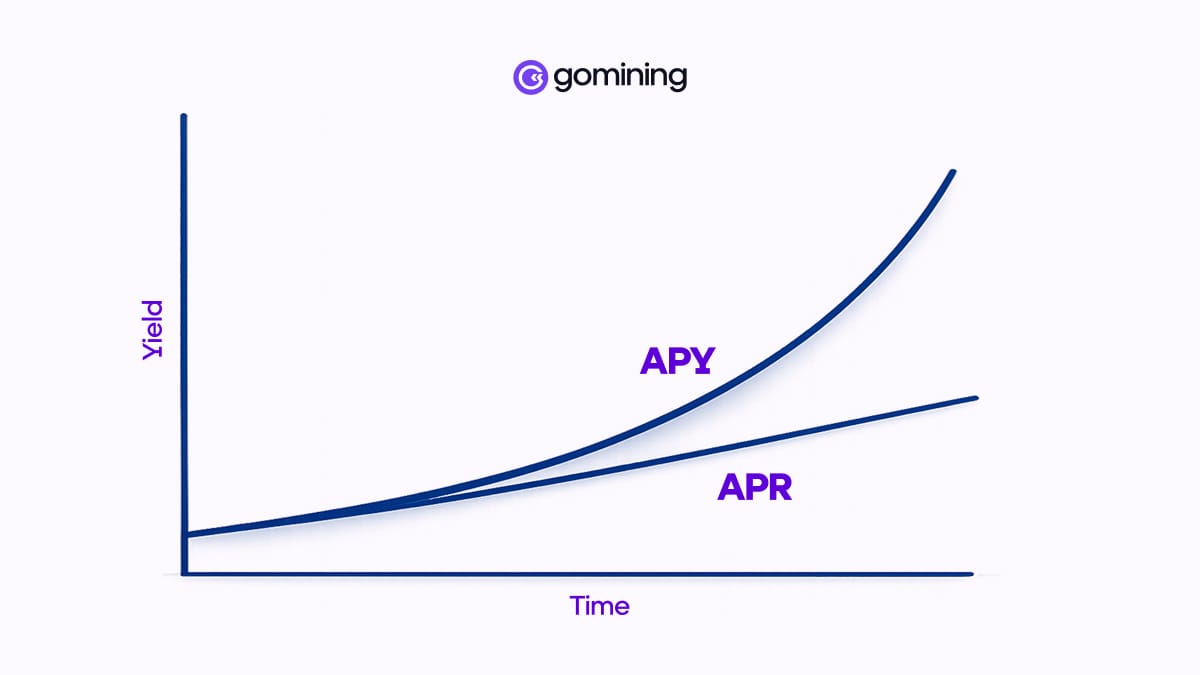

APR vs. APY in DeFi

APR

APR (Annual Percentage Rate) is the simple interest you would earn over a year without reinvesting your returns. If you deposit $100 at 12% APR, you'd earn $12 over the course of a year — straightforward, with no compounding.

APY

APY (Annual Percentage Yield) includes compounding, when your interest is added to the original amount.

Basically, your interest starts earning its own interest! For example, a 12% APR becomes roughly 12.7% APY if compounded monthly — and the gap grows much larger at higher rates. If you reinvest earnings regularly, your actual annual return can become much higher than the base APR.

Why Do DeFi Platforms Usually Show APY?

APY is always bigger. Some protocols auto-compound for you — in this case, the APY is accurate. Others, however, require you to manually reinvest your interest, so the displayed APY exaggerates what most users actually earn.

How Does Compounding Change Real Returns?

At low rates, the gap between APR and APY is small. For example, 5% APR becomes only about 5.12% APY with monthly compounding — barely noticeable. But at high rates with frequent compounding, the difference becomes enormous.

Here's why: when you're earning 100% APR and compounding daily, your returns from day 1 start earning their own returns on day 2, and so on. By the end of the year, that 100% APR can become 170% APY or higher. This is why some protocols display APYs of thousands of percent.

They're assuming you reinvest your earnings constantly — sometimes every few hours or even every block. In reality, most users don't compound that frequently (or the gas fees to do so would eat up the gains), so the actual returns end up much closer to the APR.

Real Yield vs. Inflationary Yield

Now that you understand how yield is calculated and displayed, here's a crucial question: where does the value of that yield actually come from?

Not all yield is created equal. Some comes from real economic activity that generates actual revenue. Other yield comes from simply creating new tokens and handing them out. Understanding this difference is critical — because one type tends to be sustainable, while the other often isn't.

Real Yield

Real yield comes from actual economic activity: trading fees, borrowing interest, or protocol revenue. It is backed by real demand for financial services.

Inflationary Yield

Inflationary yield comes from newly minted tokens. The protocol distributes governance tokens to users. If the token price drops as supply grows, the value of rewards decreases even while the token amount stays the same.

Why Isn’t High Yield Always Sustainable?

WARNING: A common beginner misconception is that a high percentage automatically means a great opportunity.

Here's the reality: DeFi yields above 20–30% are almost always driven by token emissions (inflationary yield) rather than actual fees or interest (real yield). The protocol is essentially printing its own tokens and giving them away to attract users early on.

First, dilution. As the protocol distributes more and more tokens, the total supply keeps growing. If demand for the token doesn't grow at the same pace, the token price falls. So even though you're receiving, say, 100 tokens per week, those tokens might lose half their value by the time you want to sell them.

Second, competition for yield. When people see high returns, more capital floods into the pool. As more users deposit funds, the same amount of rewards gets split among more people — meaning your share of the yield drops. A pool offering 100% APY with $1 million deposited might drop to 20% APY once $5 million flows in.

The result? Those eye-catching triple-digit yields rarely last more than a few weeks or months. By the time most people discover them, the best returns are already gone.

How DeFi Yield Is Paid

How Often Is Yield Accumulated?

Yield is typically calculated and added to your balance continuously, block by block — sometimes every few seconds. Your balance grows in real-time as the protocol generates fees or interest.

Keep in mind: just because yield is accumulating doesn't always mean you can access it instantly. Some protocols require a manual claim transaction to withdraw your rewards (which comes with a small gas fee).

Which Tokens Are Used to Pay Yield?

Here's something important to understand: the token you deposit and the token you earn as yield aren't always the same.

For example, you might deposit USDC (a stablecoin) into a lending pool and earn yield paid in USDC — simple as that. But in other cases, you might deposit ETH into a liquidity pool and receive the protocol's governance token as your reward instead.

WARNING: Earning in a volatile governance token is very different from earning in a stablecoin.

Here's why: if you earn 10% yield paid in USDC, you know exactly what that's worth — $10 on every $100. But if you earn 10% yield paid in a governance token, the actual dollar value of your rewards can swing wildly. That governance token might be worth $10 today and $3 tomorrow (or $20 if you're lucky). Your "10% yield" could turn into a 3% or 20% return depending on when you sell.

Always check what token your yield is paid in before depositing. A high yield paid in a declining governance token can actually result in a loss.

What Causes Yield Rates to Change?

Rates shift constantly because DeFi protocols use automated formulas that adjust yields in real-time based on supply and demand — no human sets the rates. More depositors means lower yield per person. Higher borrowing demand or trading volume pushes yield up.

Remember: DeFi NEVER offers a fixed, guaranteed rate.

Risks Behind DeFi Yield

Smart Contract Risk

DeFi runs on code. If that code contains a bug, deposited funds can be lost or stolen. Even audited protocols are not immune to such things.

Market and Price Volatility

Token values can drop while you earn yield, resulting in a net loss (when you end up with less than you had). In liquidity pools, your returns can be further reduced by impermanent loss (which happens because the ratio of tokens in the pool changes as prices move, and you end up with a different mix).

Liquidity Risk

DeFi strategies often lock your tokens for a set period — meaning you can't withdraw them even if you want to. This is common in staking or certain yield farming programs where protocols require a commitment period (like 30 or 90 days) to ensure stability. If the market crashes or the protocol encounters problems during that time, you're stuck and can't exit.

Other strategies rely on small liquidity pools with limited funds. When you try to withdraw from a small pool, there might not be enough of the token you need available at the current price. This causes slippage — the actual price you get is worse than what you expected. For example, you might think you're swapping for $1,000 worth of tokens, but due to the shallow pool, you only receive $950 worth.

Some protocols also charge early withdrawal penalties or exit fees if you try to leave before a certain timeframe. Always check if your funds are locked, how deep the liquidity pool is, and what penalties apply before depositing.

Protocol and Governance Risk

Protocols can change rules through governance votes. Reward rates can be cut, fee structures altered, or contracts upgraded in ways that affect your position.

How To Evaluate DeFi Yield Safely

What Is Generating the Yield?

Ask where the DeFi returns come from. Is it fees, borrower interest, or token emissions? A credible protocol can clearly show this.

Who Is Paying It?

If the yield is real, someone is paying for the service you provide. If you cannot identify the payer, the yield may be unsustainable.

How Long Can the Yield Realistically Last?

Governance token rewards have a limited supply of tokens. On the other hand, fee-based yield depends on continued activity. Neither is guaranteed, but fee-based yield tends to last longer.

Beginner Red Flags to Watch For

WARNING: Be cautious of any protocol offering extremely high returns without explanation, lacking a security audit, live for only a short time, or requiring locked tokens with no exit. If the yield seems too good to be true… it most probably is.

Frequently Asked Questions

Is DeFi Yield Safe for Beginners?

DeFi yield carries risks you don’t have with traditional savings. Earning Yield in DeFi starts with finding established protocols, using small amounts you can afford to lose, and learning how each protocol works before depositing more.

Why Is DeFi Yield Higher than Banks?

DeFi eliminates middlemen and operates in an open, competitive market. Higher crypto yields reflect higher risk: there is no deposit insurance, and there is no regulatory safety net.

Can Yield Change or Disappear?

Yes. A pool offering 20% today may drop to 3% next week as capital flows in or incentives expire. Never assume that current rates will last for long.

Where Should a Beginner Start?

Consider a well-known lending protocol or a stablecoin pool on a major blockchain.Focus on understanding the mechanics before chasing the highest percentage.

Key Takeaways for Beginners

DeFi yield is the return you earn for supplying crypto assets to decentralized protocols. It’s often described as DeFi passive income — only it requires monitoring due to changing rates and risks. It comes from real economic activity, such as lending interest, trading fees, and staking rewards, or from protocol token emissions that may not be sustainable.

Higher yield always means higher risk. Before depositing anything, ask what generates the return, who pays for it, and how long it can last. Remember DeFi yield basics: start small, stick with proven protocols, and treat DeFi yield as a learning experience rather than a guaranteed DeFi income stream.