What Is A High-Yield Savings Account?

It might sound weird, but most savings accounts are quietly losing you money.

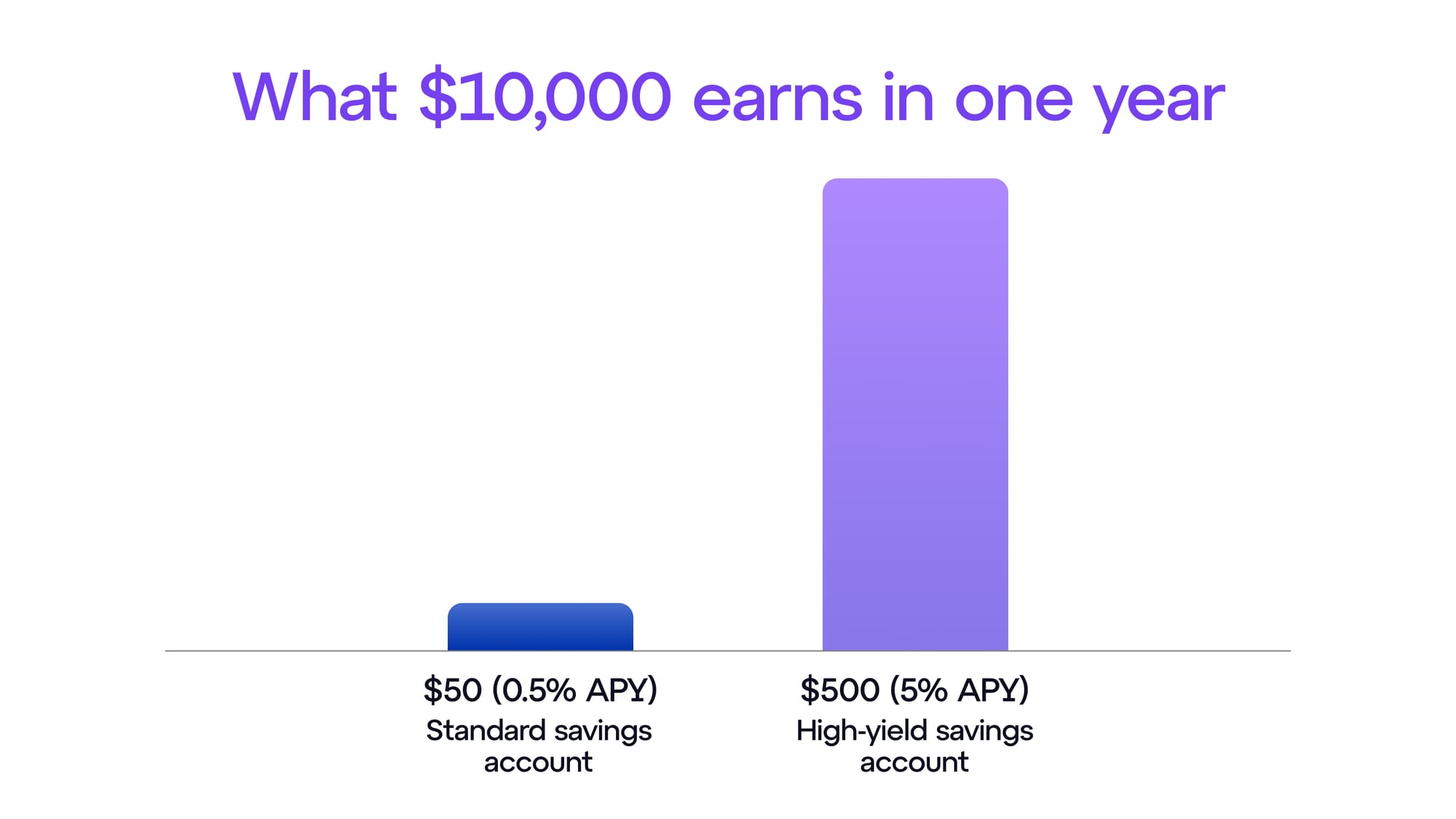

It’s not like the bank is doing anything wrong. It’s just that the interest they pay is so low that inflation eats through it faster than it accumulates. A standard savings account at a big traditional bank might earn you about 0.5% a year or even less. On $10,000, that's just $50.

A simple solution would be opening a high-yield savings account (HYSA). It's a federally insured savings account that pays significantly more interest than a traditional one, typically through an online bank. Same protection, but much better return.

Key Takeaways:

- HYSAs pay far more than traditional savings accounts, often 10–15x more, with no added risk.

- The key number to understand is APY (Annual Percentage Yield), which reflects the real return you earn after compounding.

- FDIC insurance protects your deposits up to $250,000 per account, per institution.

- Your real return is APY minus inflation minus taxes, and that number is smaller than the headline rate. That's not a reason to avoid HYSAs; just make sure to understand what you're actually earning.

- HYSAs are not a wealth-building tool on their own, but rather a foundation. It could be a place to store your emergency fund or short-term savings, while you decide what to do with money in the long term.

How A High-Yield Savings Account Works

Simply put, it’s pretty much like any regular savings account: you deposit the money, the bank pays you interest. With HYSAs, the number that matters most is the APY (Annual Percentage Yield). It tells you what you'll actually earn over a year, including the effect of compounding - the interest you earn starts earning interest, too. So the longer your money sits in the account, the larger the base it compounds on.

It's important to note that APY is different from APR (Annual Percentage Rate).

APR is used when you're the one borrowing money, like when you get a loan or a credit card. APY is what you earn when you're the one saving. For a HYSA, APY tells you what your money will actually make in a year.

You also need to ask yourself: what kind of bank is it in the first place?

Why Online Banks Pay More

There is an important difference between traditional and online banks that needs to be taken into account. A traditional bank has thousands of physical branches, staff, and real estate costs. But an online bank has none of that. With no branches to maintain, they can spend less and pass some of that saved money back to you as interest. That's the main reason online banks consistently offer higher rates.

Regardless of the type, banks will be banks, which means money in a HYSA is safe.

Your Money Stays Accessible

Your money doesn't go anywhere you can't reach it. A HYSA lets you withdraw whenever you need to. Most accounts limit you to around six withdrawals per month, but beyond that, it's liquid.

That's different from a Certificate of Deposit (CD), which locks your money away for a fixed term in exchange for a guaranteed rate. A CD might pay slightly more, but you're committing to leave the money untouched. A HYSA keeps your options open. For emergency funds or savings you might need on short notice, that matters.

What FDIC Insurance Actually Means

The Federal Deposit Insurance Corporation (FDIC) is a US government agency that insures deposits at member banks. If a bank fails, your deposits are protected up to $250,000 per depositor, per institution.

Outside the US, equivalent protections exist in most countries — the UK has the FSCS, which covers up to £85,000; the EU has deposit guarantee schemes covering up to €100,000. The names and limits differ, but the principle is the same: your deposit at an insured bank is protected.

Bank deposits are not investments. You are not buying a security or taking on market risk. Instead, you are lending money to the bank, and the government guarantees you get it back up to the coverage limit. The rate can change, but the money won’t disappear.

Outside the US, the product has different names but the same logic. In the UK, it's typically called a high-interest savings account or an easy-access savings account — offered by banks like Marcus or Chase UK, among others. In the EU, online banks and neobanks like Trade Republic or Bunq have been offering competitive rates tied to the ECB rate. The specifics vary by country, but the question to ask is always the same: what's the APY, is the bank regulated, and are my deposits insured? If the answer to all three is satisfactory, you've found the local equivalent.

What You Actually Earn: The Real Yield Calculation

And now, the main question: how much?

A 5% APY might sound good, especially compared to 0.5%. But the rate isn’t what actually lands in your pocket.

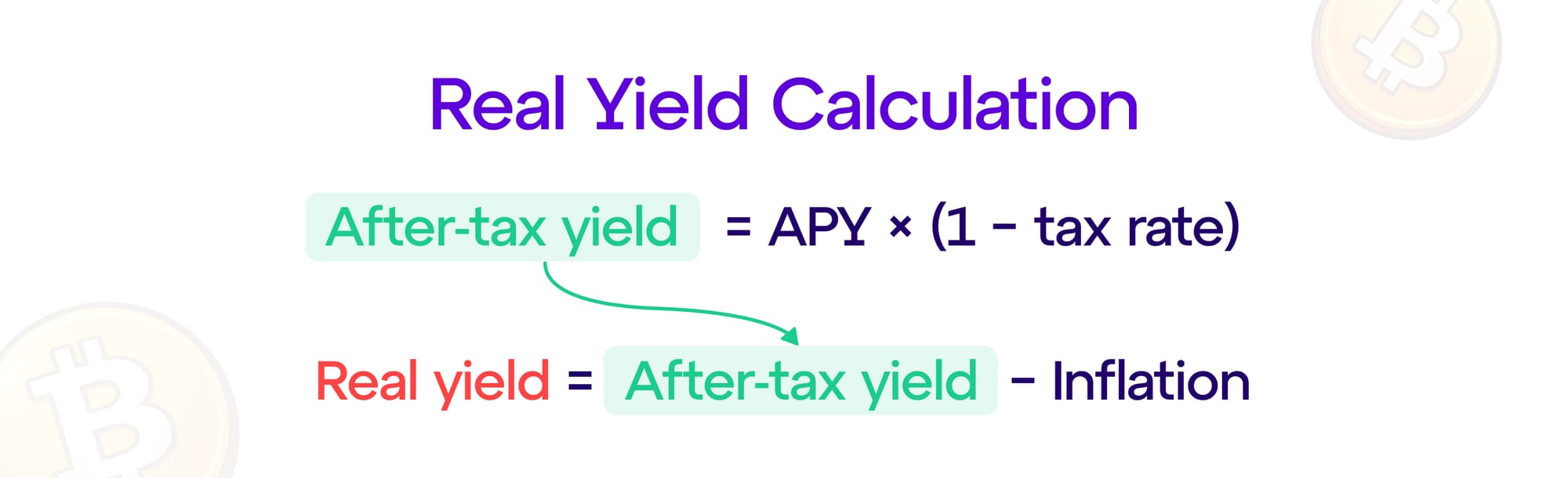

First, tax. You pay income tax on the interest you earn — not on what's left after inflation.

So the first cut is: APY × (1 − your tax rate). For example, at 5% APY and a 22% tax bracket, that leaves you with 5% × 78% = 3.9%.After-tax yield = APY × (1 − tax rate)

Then inflation. If prices rose 3% that year, subtract that from your after-tax return. You're now left with just 3.9% – 3% = 1% in real terms. So, the real yield formula is: Real yield = after-tax yield − inflation

Still, this doesn’t mean you need to avoid HYSAs. But you certainly must know what the number actually means. So, when would opening a HYSA be a good idea?

Where A HYSA Fits In The Bigger Picture

A HYSA is the right tool for a specific job: keeping money safe and accessible, and earning something reasonable while you figure out what to do with it. That’s where you would put an emergency fund — three to six months of expenses — or any other short-term savings you might need within the next year.

Think of it as your financial foundation. Before you put money into stocks, funds, or anything higher-risk, this is the floor you build on.

For longer-term goals, other options tend to outperform: stocks, index funds, real estate, crypto. Higher potential return always means higher risk and less liquidity. A HYSA trades upside for stability and instant access.If you're already in crypto and want a similar low-effort yield on assets you're holding anyway, GoMining's Simple Earn — available outside the US — works on the same principle. You activate it with a single toggle, and GoMining automatically routes your eligible crypto assets to earning protocols behind the scenes — no need for you to research, no manual management.

Yield is paid out in Bitcoin every four hours and compounds automatically. There's no lock-up: you can deposit or withdraw your funds at any time. The rate isn't fixed and isn't guaranteed — it moves with market conditions, which is a meaningful difference from a HYSA. But for crypto you're already holding, the logic is the same as a savings account: your money earns something instead of sitting still.

Risks And Limitations

Now, let’s revisit the main risks that come with HYSAs. HYSAs are about as low-risk as savings get, but they do have real limitations worth understanding.

⚠ IMPORTANT: HYSA rates are variable. They are not guaranteed. If the central bank cuts interest rates, your HYSA rate will almost certainly fall too. |

Variable rates: HYSA rates move with the broader interest rate environment. In 2022–2023, when central banks raised rates aggressively to fight inflation, HYSA rates climbed to 4–5%. When rates fall, those returns shrink. You don't lock in a rate the way you do with a bond or CD.

Inflation risk: Again, if inflation runs higher than your APY, your real purchasing power is falling even as your balance grows. This is most relevant in high-inflation environments.

Withdrawal limits: Most banks limit you to around six withdrawals per month. For an emergency fund that's rarely touched, this is fine. If you need frequent access to the money, it becomes a constraint.

Not a growth engine: At 5% APY, $10,000 earns roughly $500 in a year — that’s before you factor in tax and inflation. HYSAs just preserve and modestly grow your money — that's all they really do.

That covers the main things to know before opening one. Here are some questions that tend to come up once you start looking into it.

FAQ

Can I lose money in a high-yield savings account?

Very unlikely — at least, for what you deposit. Your interest rate can potentially change, but as long as your account is at an FDIC-insured bank (or an equivalent insured institution in your country) and your balance is within the coverage limit, your deposit is protected.

Why do HYSA rates go up and down?

Rates track the broader interest rate environment set by central banks. In the US, they follow the Federal Reserve's benchmark rate, which in turn influences the 10-year Treasury yield and the rates banks offer on deposits. When the Fed raises rates, HYSAs get more competitive. When it cuts, they follow.

Is a HYSA the same as a CD?

No. A Certificate of Deposit (CD) locks your money in for a fixed term — three months, one year, five years — in exchange for a fixed, guaranteed rate. A HYSA is flexible: you can add or withdraw money whenever you like, within monthly limits. The tradeoff is that the HYSA rate can change. The CD rate won't, however.

Do I pay tax on HYSA interest?

Yes. In most countries, interest earned on savings is taxable income. In the US, banks report it to the IRS on a 1099-INT form, and you pay ordinary income tax on it. The rate you pay depends on your tax bracket.

How is a HYSA different from investing?

A HYSA is not an investment. You're depositing money that earns a predictable return — the rate moves, but your deposit doesn’t. Investing in stocks, funds, or crypto means your balance can go up or down in value, and there's no government guarantee on what you get back. A HYSA is the alternative for money you don't want to risk.

What's a realistic amount to earn?

At 5% APY, $10,000 earns roughly $500 in a year. $50,000 earns around $2,500. These are pre-tax, pre-inflation figures. It's meaningful passive income, especially on money that would otherwise sit doing nothing.

Still have questions? GoMining Academy is a free, ever-growing collection of courses, guides, and articles on everything crypto — written for real people. No tech jargon. No prior crypto knowledge required. Start anywhere.

Telegram | Discord | Twitter (X) | Medium | Instagram