A Beginner's Guide to Crypto Taxes

It is surprising for many to learn that crypto is not tax-free.

Whether you're trading, earning, or spending digital assets, these activities often come with tax responsibilities. Governments around the world are paying closer attention, and failing to report your crypto activity can lead to costly consequences. The good news is that understanding the basics can help you stay compliant and avoid unnecessary stress.

Taxes might seem painful, but they don’t have to be boring or overly complicated or overly complicated, especially if you’re new to crypto and Bitcoin in particular.

Let’s break it down.

Table of Contents:

- Is Cryptocurrency Taxed, Really?

- When Do You Pay Taxes on Crypto

- Is Bitcoin Taxed?

- Income vs. Capital Gains (Real‑Estate Style)

- Capital Gains Corner: Do You Pay Taxes on Crypto Gains?

- Non‑Taxable Chill Zone

- Quick FAQ

- Bottom Line

- Crypto Taxes USA

- US Crypto Tax – Breakdown (Federal + State)

- Capital Gains Tax on Crypto

- Tax on Crypto Gains: Short-Term vs. Long-Term

- Reporting Requirements

- Crypto Taxes State-by-State Overview

- Are There Areas With Fewer Crypto Taxes?

- Where Crypto Taxes are Not So Great

- Important Considerations When Handling Crypto Taxes

- How to Pay Taxes on Crypto

- Conclusion

Is Cryptocurrency Taxed, Really?

Yes, in many countries you must pay tax on crypto, and ignoring it is about as smart as ignoring a toothache. Taxes are like the dental cleanings of adulthood: unavoidable, mildly uncomfortable, and always popping up when you’d rather do literally anything else.

But if you've dabbled in crypto or are a strong supporter of it, it's best to face tax season with a smile instead of a subpoena.

When Do You Pay Taxes on Crypto?

Most countries don’t see crypto as money—they see it as property, like stocks or real estate. So they don’t tax you just for owning it. They wait until you do something with it. That “something” is called a taxable event. A taxable event will either trigger an income tax or a capital gains tax fee that you will need to pay to the government.

Is Bitcoin Taxed?

Yes, Bitcoin is taxable. Bitcoin may be a permissionless digital currency, but it definitely isn’t tax-free.

How is Bitcoin Taxed?

In most jurisdictions, BTC is treated as property, so every time you sell, spend, or swap it, you trigger a capital-gains event.

Buy one Bitcoin for $20,000 and later spend it when it’s worth $30,000? That $10,000 difference is a taxable Bitcoin gain that must be reported just like a stock sale. Even non-cash moves—such as trading BTC for ETH or using it for a latte—count as taxable disposals because the government sees you “disposing” of property at fair-market value.

Mining adds another twist: block rewards arrive as ordinary income the moment they hit your wallet. The dollar value of freshly minted coins on the day you receive them is includable in your gross income—no different from a paycheck.

Later, when you eventually sell those mined coins, any price change since you first recognized them becomes a capital gain or loss that feeds into your broader Bitcoin taxes bill. In short, whether you’re cashing out at an exchange or hashing blocks in your basement, keep meticulous records. Otherwise, your crypto taxes could become a reckoning day with a painful audit.

Income vs. Capital Gains: What’s the Difference?

To go over this in clear terms:

- Income events = Collecting rent. In some countries, when you mine a block, stake tokens, or get paid in BTC, that’s like pocketing monthly rent cheques. They land in your wallet immediately and are taxable based on certain events, and thresholds, just like ordinary income at your marginal rate.

- Capital‑gains events = Flipping the house. Selling, swapping, or spending your coins is akin to handing over the deed after a remodel. Any difference between purchase price and sale price is profit that is considered taxable income. Hold more than a year and you slide into a cheaper crypto tax rate; flip in under twelve months and you pay ordinary brackets.

💥 Event | 📜 Tax Treatment | 🏠 Real Estate Comparison |

Getting Paid in Crypto | Taxed as ordinary income, based on market value at receipt | Like collecting rent—it's regular income, and it's taxable. |

Accepting Crypto for Goods or Services | Report as income based on market value at time of receipt | Payment for services? Just like rental payments—report it. |

Mining Crypto | Taxed as income at fair market value; may include self-employment tax | Like earning rental income from another property you maintain (aka your mining rig or digital miner). |

Staking Rewards | Taxed as income when received, based on fair market value | Think of it as passive rent payments; it still counts as income. |

Airdrops and Bonuses | Taxed as income at the time of receipt, based on market value | Like a surprise rent bonus from a generous tenant. Still taxable. |

Non‑Taxable Chill Zone

Buying and holding? Transferring between your own wallets? Gifting under the annual limit? No tax traction. But bookmark this page so you’ll remember how to pay taxes on crypto when you finally cash out.

Bottom Line

When crypto moons, the tax inspector follows the same trajectory. Use software to keep records, and remember: crypto and taxes go together like bricks and mortar—ignore either, and the whole house can crumble.

Crypto Tax In USA 🇺🇸

US Crypto Tax – Breakdown (Federal + State)

Perhaps you live in the United States? You might be wondering if crypto taxes in the USA are a bit different. In some ways, they are. As for July 2025, The United States treats cryptocurrency much like it treats stocks or property for tax purposes. The IRS has made it clear that crypto is taxable and is generally subject to capital gains or ordinary income tax depending on the transaction. Here’s a breakdown of how crypto taxation works at the federal level in the U.S.:

🏡 Capital Gains Tax on Crypto

Since 2014, the IRS treats cryptocurrency as property, not currency. This means:

- Selling or exchanging crypto is like selling a house or stock.

- Profits from these sales are capital gains.

- Losses can offset other gains or reduce taxable income.

💰Tax on Crypto Gains: Short-Term vs. Long-Term

- Short-Term Gains (held ≤ 1 year): Taxed as ordinary income (10%–37%).

- Long-Term Gains (held > 1 year): Taxed at reduced rates (0%, 15%, or 20%) depending on income.

🛠️ Crypto as Income

Earning crypto? It's considered income if you:

- Get paid in crypto for work.

- Mine or stake coins.

- Receive airdrops.

Report the fair market value at the time of receipt as income and pay tax on it. Later, if you sell at a higher price, that's a capital gain, and must pay capital gains tax on it.

🚫 Non-Taxable Events

- Buying and holding crypto.

- Transferring crypto between your own wallets.

- Gifting crypto (within limits)

- Donating crypto to qualified charities.

📝 Reporting Requirements

- Form 1040: Answer the digital asset question.

- Form 8949 & Schedule D: Report capital gains and losses.

- Schedule 1 or C: Report crypto income.

Starting in 2025, brokers will use Form 1099-DA to report crypto sales to the IRS.

🗺️ Crypto Taxes State-by-State Overview

Beyond federal taxes, U.S. crypto investors may also face state taxes, which is where things vary significantly depending on where you live. The U.S. has a mix of states with different income tax rules, and since some crypto earnings often count as income for state purposes, your state of residence can affect your total tax bill. Here are some key points on how states differ:

🌞 States with No Income Tax

As of July 2025, residents owe no state tax on crypto:

- Florida

- Texas

- Wyoming

- Nevada

- South Dakota

- Alaska

- Washington*

- Tennessee

- New Hampshire

*Note: Washington imposes a 7% tax on long-term capital gains over $250,000, including crypto taxation.

🌧️ States with High Income Taxes

States like California, New York, and Hawaii tax crypto gains at higher rates:

- California: Up to 13.3% on income, including crypto gains.

- New York: Up to 10.9% state tax, plus NYC tax if applicable.

- Hawaii: Up to 11% on income, with specific rates for capital gains.

⚠️ Special Considerations

- Massachusetts: Short-term gains taxed at 8.5%; long-term at 5%.

- Colorado: Allows state tax payments in crypto.

- Wyoming: Recognized for crypto-friendly regulations and no state income tax.

Key Takeaways

- Federal Level: Crypto that is sold is taxed as property; gains and income must be reported.

- State Level: Tax treatment varies; some states offer significant savings.

- Compliance: Use crypto tax software or consult a tax professional to ensure accurate reporting.

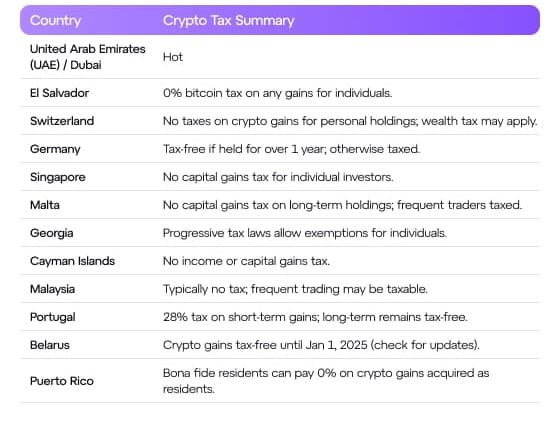

✈️ Countries with Fewer Crypto Taxes

As of July 2025, here are some countries that are often cited for favorable or 0% tax on cryptocurrency sales, with important caveats:

Where Crypto Taxes Are Not So Favorable

And after discussing the countries where crypto taxes are not so bad, it is time for a brief list of places where if you deal with crypto, life might not be so great from a crypto taxes perspective.

Crypto Taxes in India

- Since 2022, India hits every crypto profit with a flat 30% tax. That’s right—no matter how big or small, if you made a gain, your cryptocurrency tax rate is 30%.

- No loss offsets allowed: Did you lose money on another coin and hope to balance things out? Well, losses can’t be deducted—not from other crypto gains, not from anything. A loss is just... a loss.

- Plus, there's a 1% TDS (Tax Deducted at Source): Every time you sell, swap, or transfer crypto, 1% is automatically deducted—even if you made no profit.

- The goal: These strict rules were designed to cool down speculation.

- There’ve been calls to ease the rules, but as of 2025, they’re still in place. So if you’re a crypto investor in India, you’ll want to plan carefully—and maybe keep a good tax advisor on speed dial.

How Is Crypto Taxed in the UK?

- If your profits are small, you're in luck. Everyone gets a tax-free allowance on capital gains—though it's been shrinking fast. As of 2025, the tax-free allowance is just £3000 If your total crypto profits stay under that, you don’t owe a penny in capital gains tax.

- Once you go over the allowance, your gains get taxed at either 10% (basic income level) or 20% (higher income level). Crypto from mining, staking, or being paid in it is treated like regular income—so you’ll pay income tax based on your bracket.

- Paperwork Patrol: The UK takes tracking seriously. You’re expected to keep detailed records of every crypto transaction—buys, sells, swaps, even gas fees. HMRC wants the receipts. 🧾

- The UK is okay for casual hodlers with small gains. But if you’re making serious moves, expect taxes—and lots of record-keeping.

Crypto Taxes in Canada

- Canada taxes only 50% of your crypto capital gains. So if you made $10,000 in profit, you only get taxed on $5,000 of it. That’s a win compared to countries that tax 100% of your gains.

- If you trade frequently or make it your “business,” the tax office (CRA) might treat your profits as business income, which is fully taxed at your regular income tax rate Also, using crypto to buy something (like coffee) counts as selling it—so you may owe tax on any gains, even for small purchases.

- Canada is moderately strict in terms of taxes, if you’re a casual investor holding for the long term. But if you’re flipping coins like pancakes, it can get expensive tax-wise.

Important Considerations When Handling Crypto Taxes

- Individual vs. Business: Many of these favorable tax regimes apply primarily to individual investors who are not engaging in frequent, high-volume trading as a business. If cryptocurrency activities are considered a business, income tax or corporate tax may apply.

- Holding Period: The length of time you hold your cryptocurrency can significantly impact its tax treatment in some countries.

- Type of Crypto Activity: Whether you are simply buying and holding, trading, mining, staking, or earning crypto as income can affect how it is taxed.

- Residency: To benefit from a country's tax laws, you typically need to establish tax residency there, which involves meeting specific criteria.

- Changing Regulations: Cryptocurrency tax laws are constantly evolving. It's crucial to stay updated on the latest regulations in any country you are considering.

- Professional Advice: Due to the complexity and variability of these laws, it is always highly recommended to consult with a tax professional specializing in cryptocurrency before making any financial or relocation decisions. You could use a reputable crypto tax calculator to give you a rough estimate, but expert consultation is always a priority.

How to Pay Taxes on Crypto

- Export every trade into a CSV

- Consult with a tax professional

- Separate every taxable crypto disposal into two “buckets”

- Short-term — coins you held one year or less before you sold, spent, or swapped them

- Long-term — coins you held for more than one year

- File Form 8949 (U.S.) or your country’s equivalent

- Budget that fiat currency to pay the tax authority; penalties snowball faster than a memecoin pump

Conclusion

Tax on cryptocurrency is a moving target. Governments are continually updating regulations as the crypto market evolves. In conclusion, the trend is toward greater clarity and enforcement of crypto taxes worldwide.

This is because cryptocurrencies are a global phenomenon, unlike regional fiat currencies. The silver lining is that as rules get clearer, it may become easier to comply (with official forms, standardized rules, etc.)

For now, if you’re a crypto holder, stay informed each tax year about new developments – whether it’s a new form from your exchange, a proposed law that could affect your strategy, or a change in your country’s tax rates or exemptions.